|

Table 1: India’s top 10 crude oil suppliers |

|

Country |

Supply (Barrels/Day) |

Shipping Days |

Major Crude Grade |

Category |

Currency |

|

Russia |

1.1–1.6 million |

25–35 days |

Urals, |

Sour |

Rubles/ Yuan / Dirham / USD |

|

Iraq |

850k–900k |

5–7 days |

Basrah Medium, Basrah Heavy |

Sour |

USD |

|

Saudi Arabia |

600k–700k |

6–8 days |

Arab Light, Arab Medium |

Sour |

USD |

|

UAE |

400k–450k |

3–5 days |

Murban, Upper Zakum |

Sweet, Sour |

USD / Dirham |

|

United States |

450k–550k |

35–45 days |

WTI, Eagle Ford |

Sweet |

USD |

|

Kuwait |

300k–350k |

5–7 days |

Kuwait Export Crude |

Sour |

USD |

|

Nigeria |

120k–180k |

20–24 days |

Bonny Light, Qua Iboe |

Sweet |

USD |

|

Angola |

100k–120k |

18–22 days |

Girassol, Dalia |

Sweet, Sour |

USD |

|

Brazil |

80k–100k |

30–35 days |

Lula, Tupi |

Sweet |

USD |

|

Mexico |

70k–90k |

35–40 days |

Maya |

Sour |

USD |

Source: Author’s compilation based on IEA, PIB, and media reports

Due to its geographical location far from the disruption, the US has emerged as an alternative supply source. However, long shipping distance increases freight charges, transit time and insurance premiums. US crude is also more expensive making it an unattractive choice as costly energy alternatives would widen India's current account deficit, weaken the rupee, raise inflation, affect monetary policy as well as fiscal management. Similar bottlenecks evolve when crude oil is brought from Latin American countries like Brazil, Guyana, or West African producers such as Nigeria and Angola. Although these routes bypass the strait of Hormuz, hold low geopolitical risk and strengthen supply resilience, and serve as alternatives to traditional West Asian energy dependence during periods of instability, longer transportation distances reduce their overall competitiveness. In addition, as visible from Table 1, at present, the combined import from these suppliers does not equal to the crude imports from Russia and West Asian countries.

An additional structural limitation arises from refinery compatibility. Indian refineries are optimized to process medium-to-heavy sour crude oil, capable of processing heavier and more sulfur-rich crude efficiently and convert lower-cost crude into high-value fuels. Such a limitation poses an obstacle in replacing the Arab countries or Russia with the US that produce light sweet crude oil namely Brent Crude Oil and West Texas Intermediate which are less compatible with India’s existing refining configuration. Processing such crude requires blending with heavier grades, reducing operational efficiency and increasing refining costs.

Furthermore, dependence on the petrodollar system for crude oil trade continues to further constrains energy security. Since crude oil trade is predominantly conducted in U.S. dollars, fluctuations in the rupee-dollar exchange rate directly influence import costs and domestic fuel prices leading to inflationary pressures. Dollar-denominated trade also exposes India to secondary sanctions and financial pressure linked to geopolitical alignments, particularly when importing crude from countries viewed unfavorably by Washington. As a result, despite diversification efforts, India’s energy sector remains vulnerable to external financial and geopolitical disruptions.

Spot trading as an option

Spot trading of crude oil is a mechanism rather than an alternative to mitigate the market volatility that occurred due to geopolitical events, shipping disruptions, natural disasters, OPEC+ decision or economic trends. Traders and governments use spot trading to hedge risk, diversify supply portfolios, and secure short-term procurement opportunities during periods of uncertainty. Crude oil is brought or sold for immediate delivery reflecting prevailing market demand and supply conditions. Commonly described as trading “on the spot”, it represents the current market value of oil and is heavily influenced by short-term fluctuations in supply and demand.

Current development in west Asia and the de facto blockade of Strait of Hormuz leading to restriction of shipping has activated spot markets as a mechanism for immediate and flexible procurement of crude oil from non-Arab sources. Spot procurement enables India to maintain supply continuity despite disruptions in traditional shipping routes.

Despite its operational advantages, India cannot heavily rely on spot trading as it carries inherent economic and strategic risks. Spot markets are more volatile because prices fluctuate in response to immediate supply and demand dynamics, shipping availability, and benchmark price movements. Frequent dependence on spot purchases can therefore increase India's import costs and fiscal stability. Thus, spot trading must primarily be utilised as a short-term supply management tool rather than a long-term solution to such geopolitical events. While spot markets provide flexibility during emergencies, they do not eliminate India's exposure to maritime chokepoints and regional instability.

Pipelines to bypass the Strait

Another available infrastructural option that can support recourse from the Strait of Hormuz is the utilization of pipelines in West Asia. Saudi Arabia operates the East–West Pipeline (Petroline), connecting the oil - rich Abqaiq field in the Eastern Province to the port of Yanbu overseeing the Red Sea (Arab News, 2026). The UAE has constructed Abu Dhabi Crude Oil Pipeline (ADCOP), linking inland oil fields at Habshan to the port of Fujairah on the Gulf of Oman (Abu Dhabi National Oil Company, 2021). Oman has a main oil pipeline in Oman that runs approximately 250 kilometers from the Fahud oilfield to the Mina al Fahal coastal terminal in Muscat. The pipeline will be connected to the proposed 440 Km Ras Markaz pipeline extending till the Ras Markaz Oil Storage Terminal in Duqm (Oman Ministry of Energy and Minerals, 2020).

However, the capacity at which these pipelines operate are limited. For example, Saudi Arabia’s East-West Pipeline can transport only 7 million barrels a day which only partially offsets the loss of the 15 million barrels that normally pass through the Strait of Hormuz (EIA, 2023). Similarly, The UAE ADCOP only operates 1.8 million barrels per day (Abu Dhabi National Oil Company, 2021). While these pipelines can absorb a portion of the shipment that usually go through the strait, their combined capacity is only about 9 million bpd, compared to 20 million bpd that flow through the strait. Dingli (2012) also supports this argument in his work where he states that pipelines that would carry only a drop of China’s oil demand. Thus, the pipelines would support the crude oil prices from skyrocketing in times of geopolitical crisis. However, due to their structural limitations, pipelines cannot be termed as an alternative.

Pipelines are also vulnerable to attacks during periods of conflict. In May 2019, the Saudi energy ministry reported that the East–West pipeline had been struck by drones launched by Yemen’s Houthi militia (Gornall, 2024). More recently, in March 2026, a fuel storage tank at the port of Duqm in Oman was reportedly targeted by Iranian drones for hosting a U.S. military vessel (Varghese, 2026), underscoring the exposure of pipelines associated with ports in conflict zones. The incident highlights the facts that pipelines constitute critical infrastructure and are easily targeted in times of a conflict. Being within the range of Iranian missiles and drones, makes them just as vulnerable to attacks and damage as ships travelling through the strait.

Reliance on Domestic Gas production

To diversify reliance on imported LNG, the Government of India is encouraging domestic gas production, promoting Compressed Bio-Gas (CBG) and increasing output from the KG-D6 basin. In addition, substitute energy sources such as fuel pellets, coal, kerosene, and biomass are also promoted. However, projections indicate that LNG and LPG demand will rise sharply in the near future, while domestic production is expected to grow only marginally (IEA, 2025). The alternatives promoted also pose public health risks due to higher emissions and indoor air pollution.

This study evaluates India’s alternative energy options through a comparative analysis framework based on four criteria: supply reliability, economic viability, geopolitical risk, and long-term sustainability. Each alternative is assessed according to its ability to maintain uninterrupted energy flow during a prolonged Hormuz disruption while minimizing any vulnerability.

Table 2: Comparative evaluation of available alternatives

|

Option |

Reliability |

Cost |

Risk |

Sustainability |

Overall Assessment |

|

Existing reserves |

Exhaustive and dependable for only immediate crisis management |

Low transportation and distribution cost compared to imports |

No associated risk |

Very Low |

Current reserves are low to sustain India’s energy demands |

|

Russian crude |

Highly reliable. Russia is second highest supplier |

Cheaper than other sources |

Sanctions from US |

Depends on Geopolitical events. |

Viable for short period |

|

Diversified supply |

Reliable as supply continuity is ensured |

High due to costlier insurance premiums |

Low |

Not sustainable as Current Account Deficit rises for the long run |

Emergency option |

|

Spot trading |

Lowest reliability |

Very high and unstable |

Market volatility |

Low |

For Crisis management only |

|

Pipelines bypassing Hormuz |

Short time reliability |

Changes as per location |

Prone to attack |

Sustainability depends on Infrastructural exposure |

Supportive measure and not an alternative |

|

Domestic production |

Reliable for short period till the demand exceeds production |

Comparatively cheaper to imports |

Environmental effects and public health risk |

Sustainable only when produced with low carbon footprints |

The best alternative to reduce energy import dependence if the risks associated with it is negated. |

Source: Compiled by author

The comparative analysis demonstrates that no single known alternative can fully pose as a substitute and resolve India’s long-term energy insecurity. Furthermore, growing competition among Asian economies for the same alternative supply sources reduces the reliability and attractiveness of these options during perods of crisis. This necessitates an approach combining multiple options and supply channels to ensure resilience during geopolitical disruptions. The alternatives discussed above can only serve as short – term solutions to energy disruptions.

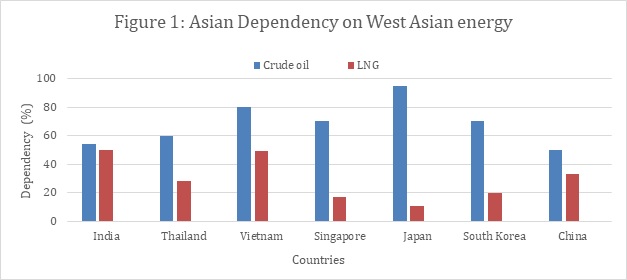

Regional competition for energy

Supply disruption due to the blockade of the strait of Hormuz has intensified competition between Asian economies for alternative energy supplies. More than half the amount of crude oil that moves through the Strait towards Asia are destined to China, India, Japan, and South Korea. Recent trends show that several south east Asian nations such as Philippines, Thailand and Vietnam are eyeing Russian crude. Such high demand for discounted Russian crude could affect Indian imports. The Philippines, for example, imported Russian crude for the first time in five years shortly after declaring an energy emergency. Japan, South Korea, and Southeast Asia have also begun sourcing crude from the United States, West Africa, and South America. However, due to freight cost and increasing crude oil prices poorer Asian nations are scrambling for nearby sources. The blockade has also caused intense competition among Asian countries for Natural Gas. Such demand has forced importers like China, Japan, and India to battle for spot LNG cargoes.

Source: The author has collected data from various online reports

Table 3: India’s regional energy competition and implications

|

Energy |

Nature of Competition |

Implication for India |

|

Russian crude |

High demand for discounted crude |

Reduced availability and higher prices for India |

|

United States LNG and crude |

Strong purchasing power of these countries and long-term LNG contracts |

Transit time to India is more |

|

African crude |

Increased imports by other countries |

Spot trading difficulty |

|

Latin American crude |

Growing demand from Asian economies |

Supply competition and long distant freight challenges |

|

Australian LNG |

Long term contracts with East Asia countries |

Limited spot cargo availability for India |

Source: Compiled by the Author

Solutions to India's energy question

Since the alternatives such as existing reserves, Russian crude, supply diversification, spot trading and domestic production function as short-term solutions for immediate crisis management remain vulnerable to geopolitical competition, India requires a phased strategic framework to achieve energy resilience. The medium- and long-term solutions to address India’s energy demands are discussed below.

Medium-Term Strategies

Increase strategic reserve

Among the possible solutions that can be adopted, one key component is the strategic petroleum reserve (SPR). While strong economies of the world hold reserve above 100 million barrels, India’s existing SPR capacity is only about 39.36 million barrels (PIB, 2023). Enhancing strategic reserve capacities, irrespective of the current West Asia crisis and the blockade is important for buffer against supply shocks and India's energy security.

Similarly, India currently operates only underground LPG storage caverns in two states with a combined capacity of approximately 1.6 lakh tonnes, equivalent to roughly two days of national consumption (PIB, 2023). Conversely, Japan maintains an LPG stockpile of 90 days reflecting higher levels of preparedness against supply shocks. Japan holds the world’s largest liquefied natural gas (LNG) storage capacity. The infrastructure is supported by an extensive network of both underground and above-ground cryogenic storage facilities designed to be highly disaster-resilient, integrated with artificial intelligence (AI) and Internet of Things (IoT) technologies. India could benefit from adopting best practices from Japan.

Multilateral mechanism for diplomatic negotiation

Importing countries not participating in the conflict should negotiate arrangements with Iran to ensure the safe passage of tankers carrying oil and gas through the Strait. A coordinated regional diplomatic response could provide an additional layer of risk mitigation. Countries that are non-aligned or not directly involved in the conflict could form a coalition or regional grouping/ multilateral mechanism to engage in dialogue with both Iran, Israel and the United States to ensure the continued flow of energy through the maritime chokepoints. Further, the multilateral institution could engage in any such future conflict where energy flow is disrupted and ensure smooth supply.

Utilising state - of - the art refineries for South American crude

Indian refiners have recently resumed importing Venezuelan crude oil after a period of suspension which were influenced by U.S. sanctions. Venezuelan crude oil such as Maya and Merey are heavy sour crude oil, which has both high density and high sulfur content. Due to its thickness and viscosity, it requires more advanced and energy-intensive refineries to convert it into usable fuels that are also more difficult and expensive to refine. Brazil, Canada, and Mexico also produce similar heavy crudes. While most of the crude oil importing countries lack sophisticated refineries in place, Indian refineries are configured to refine such heavy crude. For example, Reliance’s Jamnagar refinery has a Nelson Complexity Index (NCI) of 21.1, which is the highest in the world reflecting advanced capability to process heavy crudes to high end valuable products. [2] However, being located 9800 nautical miles across the world, crude shipments from Venezuela and other South American producers typically require voyages of around 40 days to reach Indian ports. Consequently, high freight charges increase crude price rises to $4 per barrel. Nevertheless, when offered at a sufficient discount, importing Venezuelan crude can remain economically viable for Indian refiners. Securing access to discounted crude for long term ensures a more stable and continuous flow of crude oil that provides India with greater leverage in global energy markets while reducing vulnerability to supply competition from other major importing nations.

Currency swap agreement

Currency swaps agreements refer to exchange of one currency for another at a preset rate over a given period involving two parties/countries. India currently holds such mechanism based crude trade agreements with Russia and the United Arab Emirates. These arrangements are intended to reduce exposure to exchange-rate volatility, mitigate the risks associated with overdependence on the U.S. dollar, and enhance financial resilience in energy transactions during periods of geopolitical uncertainty. Going forward, India should encourage energy trade with its diverse supplier base through a flexible payment framework that combines local currencies with the U.S. dollar. Such a hybrid settlement mechanism would preserve the stability and global acceptance of the dollar, reducing vulnerability to sanctions and currency fluctuations.

Turning to the swing producers

A swing producer is one that “has a large market share, spare capacity, very low production costs, and is capable of raising and lowering production to affect the price” (Coy, 2015). Historically, Saudi Arabia fell in this definition and had spare capacity of more than 1.5 - 2 million barrels per day. Today, outside of West Asia, the United States, Canada, Guyana and Brazil have significant crude oil production capacity capable of acting as a swing producer by increasing output quickly to offset supply disruptions within 30 to 90 days. (EIA, 2025) Russia also has a limited, yet emerging, potential to act as a swing producer. A long - term pre-arrangement with such a “crisis ready” or swing supplier can avoid the disruptions caused by geopolitical tension. Such agreements can serve as a cushion against forcing India into spot trading. A preplanned agreement should allow the swing producer to allocate spare production capacity to India during emergencies mitigating the competitive pressures India faces from other major Asian crude oil importers.

Long- term strategy

Looking East

The proven oil reserves of Southeast Asia are around 16 billion barrels, approximately 1% of the world reserves and 39% of the Asia-Pacific reserves (Cu, Phung, & Le, 2018). Due to lack of refining capacity, these countries are forced to import refined petroleum. Indonesia produces approximately 608,100 barrels of crude oil per day. However, domestic consumption is estimated at around 1.6 million barrels per day (Hanan,2025), highlighting a substantial gap between production and demand. Despite being the third-largest oil producer in the Asia–Pacific region, Indonesia remains heavily dependent on imported refined petroleum products. This is due to the country's aging refineries. Consequently, a substantial portion of its refined fuel supply is sourced from Singapore, the largest refining hub in Southeast Asia but for high cost. Similarly, Malaysia with the highest capacity of proven reserves in Southeast Asia, is a significant exporter of crude and importer of petroleum products.

One potential strategy could involve trading refined petroleum products from India in exchange for crude oil from Indonesia. India has emerged as a major global hub for refined petroleum products, exporting approximately $65.4 billion worth of refined fuels in 2024, thereby becoming the world’s second-largest exporter of refined petroleum. This strong downstream capacity provides India with an advantage in regional energy markets. Building on this strength, India could establish a structured exchange of refined products for crude utilising India's diversified supply base who are net exporters of crude but importers of refined petroleum. India must tap this gap by increasing its refining capacity. The strategy could be slowly implemented across the ASEAN countries who depend on Singapore for refined products at higher cost.

Furthermore, Indonesia is considered one of the most promising countries for petroleum investment due to its large number of sedimentary basins and established infrastructure. The country contains more than 60 sedimentary basins, many of which remain underexplored or undeveloped (Cu, Phung, & Le, 2018). The country's regulatory framework allows international companies to participate in investment and exploration of these sites. India could therefore participate in exploration of these basins and production of oil by facilitating upstream investment through ONGC Videsh Limited.

Another potential strategy is establishing a refining infrastructure in the Andaman and Nicobar Islands which could provide several advantages including proximity to Southeast Asia, reduced transportation time and shipping costs and capacity to export refined products to ASEAN markets.

New partners for LNG security

As India’s demand for natural gas continues to rise, India must strategically position itself in the global gas markets by establishing long-term energy linkages particularly looking at the future geopolitical dimensions.

Malaysia is among the top five global producers and exporters of liquefied natural gas (LNG), with annual production estimated at approximately 70–75 billion cubic meters (IEA, 2024). The country exports around 26–27 million tonnes of LNG annually, primarily under long-term, high-value contracts with major Asian consumers such as Japan and South Korea. India’s LNG imports from Malaysia remain minimal at present. Nevertheless, Malaysia could serve as a viable alternative supplier capable of providing reliable LNG volumes under flexible contractual arrangements. A key advantage is the relatively short shipping duration between Malaysia and India, typically 3-4 days, which enables rapid delivery. Malaysia’s location far away from the West Asian crisis also makes it a reliable source.

Another pillar of India’s LNG diversification source could be Australia which ranks among the top three global LNG exporters. LNG shipments from Australia to India generally take around 9 days and with large-scale LNG projects such as Gorgon, Wheatstone, and Prelude consistent production capacity can be assured.

Alternative domestic production methods

Adopting unconventional sources of natural gas, particularly Coal Bed Methane (CBM), which is extracted from coal seams could serve as a supplementary source of domestic gas and contribute to reducing import dependence over the long term. The Ministry of Petroleum and Natural Gas has launched Mission Anveshan, a programme for conducting 2D seismic surveys across uncharted onshore sedimentary basins, targeting over 20,000-line kilometres of survey data in seven priority basins (AGGRP, 2025). As an extension of the National Seismic Programme (NSP), the initiative aims to identify untapped hydrocarbon reserves in underexplored basins that collectively hold a significant portion of India’s estimated 42 billion tonnes of hydrocarbon resources (AGGRP, 2025). The program supports efforts to reduce the energy trade deficit and enhance long-term energy availability. At current consumption levels, these reserves are estimated to provide roughly 22 years of supply.

Blending programme

India’s existing Ethanol Blending Programme (EBP) represents an ambitious strategy to enhance energy security by reducing dependence on crude oil imports. Under the programme, the Government has set a target of achieving 20 percent ethanol blending in petrol by 2030. The initiative has progressed rapidly, with ethanol blending in petrol increasing from 1.53 percent in 2014 to over 19 percent by August 2025 (Government of India, 2025), highlighting significant improvements in its implementation. A similar blending programme could be explored for liquefied petroleum gas (LPG) and other gaseous fuels. In addition to expanding supply sources and domestic production, the Government could consider promoting Dimethyl Ether (DME) as an alternative clean-burning fuel. DME is produced through the dehydration of methanol in the presence of a catalyst, with coal and biomass serving as key feedstocks for methanol synthesis (CSIR, n.d.). DME could then be blended with liquefied petroleum gas (LPG) at levels of up to 20 percent without requiring major modifications to existing infrastructure or distribution systems which could facilitate its gradual adoption in the household cooking fuel sector. This blending strategy could reduce import dependence, and promote the use of domestically sourced energy resources.

Conclusion

The blockade of the Strait of Hormuz demonstrated that India’s upstream energy supply remains highly vulnerable to geopolitical supply shocks, exposing structural weaknesses rooted in external dependence. Though switching towards renewable sources of energy is the best alternative, the transition cannot be rapid but a gradual process. To mitigate the risks associated with its heavy dependence on imports, India should maintain a multi-layered energy security strategy. India must take a flexible energy procurement stance that can adjust based on changing circumstances switching sources simultaneously delineating the cost and time. For this India must hold an energy buffer and several alternatives and wide supply sources that would act as a cushion in times of sudden supply shocks emerging due to geopolitical tensions.

[1] A Traffic Separation Scheme (TSS) is maritime traffic routing system designed by IMO to avoid collision and enhance safety

[2] The Nelson Complexity Index (NCI) is a metric that measures an oil refinery's secondary conversion capacity compared to its primary distillation capacity, developed by W.L. Nelson. It ranks refinery sophistication and value-addition potential, with higher values (e.g., >10) indicating advanced abilities to process heavy/sour crude into valuable products.

References:

Abraham, R. (2013). Closure of the Strait of Hormuz: Possibilities and challenges for India. Air Power Journal, 8(1), 117–136. New Delhi: Centre for Air Power Studies.

Abu Dhabi National Oil Company. (2021). Abu Dhabi crude oil pipeline (ADCOP). Abu Dhabi, United Arab Emirates.

AGGRP. (2025). Anveshan: Seismic survey incentivization programme to boost India's energy security. Retrieved on April 3, 2026 from https://aggrp.in/anveshan-seismic-survey-incentivization-programme-to-boost-indias-energy-security/

Brito, D. L., & Jaffe, A. M. (2010). Reducing vulnerability of the Strait of Hormuz. James A. Baker III Institute for Public Policy, Rice University. Houston, TX.

Centre for Research on Energy and Clean Air. (2026, January 13). December 2025 monthly analysis of Russian fossil fuel exports and sanctions. Retrieved on April 3, 2026 from https://energyandcleanair.org/december-2025-monthly-analysis-of-russian-fossil-fuel-exports-and-sanctions/

Coy, P. (2015, December 9). Shale doesn't swing oil prices—OPEC does. Bloomberg.

Council of Scientific and Industrial Research (CSIR). (n.d.).

Dimethyl ether (DME) process technology: An ultra-clean fuel.

Retrieved on April 8, 2026, from https://www.csir.res.in/en/csir-success-stories/dimethyl-ether-dme-process-technology-ultra-clean-fuel

Cu, M. H., Phung, K. H., & Le, H. A. (2018). An overview of petroleum potential and investment opportunities in Southeast Asia. Journal of Asian Scientific Research, 8(5), 236–247.

Federal Reserve Bank of Dallas. (2026, March 20). What the closure of the Strait of Hormuz means for the global economy. Retrieved on March 24, 2026 from https://www.dallasfed.org/research/economics/2026/0320

Global Witness. (2026, March 3). Why the US and Israel attacked Iran, and what it means for oil. Retrieved March 25, 2026 from https://globalwitness.org/en/campaigns/fossil-fuels/why-the-us-and-israel-attacked-iran-and-what-it-means-for-oil/

Gornall, J. (2024). How Saudi Arabia's East-West pipeline is easing the strain on the Strait of Hormuz. Arab News. Retrieved on March 31, 2026, from https://www.arabnews.com/node/2638351

Government of India. (2021, February 3). Strategic crude oil reserves. Retrieved March 24, 2026, from https://www.pib.gov.in/PressReleasePage.aspx?PRID=1694712

Government of India. (2023, August 3). Strategic petroleum reserve programme. Retrieved March 28, 2026, from https://www.pib.gov.in/PressReleasePage.aspx?PRID=1945418

Government of India. (2025, August 11). Government speeds up ethanol blending with expanded production and infrastructure. Press Information Bureau. Retrieved on April 8, 2026 from https://www.pib.gov.in/PressReleasePage.aspx?PRID=2155110&utm_source=chatgpt.com®=3&lang=2

Government of India. (2026, March 11). Inter-ministerial briefing held on recent developments in West Asia: 70% of India’s crude imports now routed outside Strait of Hormuz; energy supplies remain secure. Press Information Bureau Retrieved on April 3, 2026 from https://www.pib.gov.in/PressReleasePage.aspx?PRID=2238525

Hanan, A. (2025, October 6). Why oil-rich Indonesia imports most of its fuel. Asia Times. Retrieved from https://asiatimes.com/2025/10/why-oil-rich-indonesia-imports-most-of-its-fuel/

International Atomic Energy Agency. (2025). Verification and monitoring in the Islamic Republic of Iran in light of United Nations Security Council resolution 2231 (2015). Vienna: IAEA.

International Energy Agency. (n.d.). Energy security. Retrieved April 6, 2026, from https://www.iea.org/glossary

International Energy Agency. (2024). Gas market lessons from the 2022–2023 energy crisis. Retrieved on April 3, 2026 from https://www.iea.org/reports/gas-market-lessons-from-the-2022-2023-energy-crisis

International Energy Agency. (2026, February 6). Strait of Hormuz. Retrieved on March 23, 2026 from https://www.iea.org/about/oil-security-and-emergency-response/strait-of-hormuz

International Maritime Organization. (n.d.). Convention on the International Regulations for Preventing Collisions at Sea (COLREG), 1972. Retrieved April 5, 2026, from https://www.imo.org/en/about/conventions/pages/colreg.aspx

Khamenei, A. (2025, June 4). Speech on nuclear negotiations and uranium enrichment. Tehran, Iran. Retrieved on March 22, 2026 from https://www.aljazeera.com/news/2025/6/4/irans-khamenei-slams-us-nuclear-proposal-vows-to-keep-enriching-uranium

Khan, A. (2026, March 28). The real cost of maritime conflict in the Strait of Hormuz: Implications for India’s security of energy. National Maritime Foundation. Retrieved on April 3, 2026 from https://maritimeindia.org/the-real-cost-of-maritime-conflict-in-the-strait-of-hormuz-implications-for-indias-security-of-energy/

Meredith, S., Shan, L. Y., & Kimball, S. (2026, March 22). Oil prices are set to rise further as war in the Middle East escalates. CNBC. Retrieved on April 5, 2026 from https://www.cnbc.com/2026/03/22/oil-prices-are-set-to-rise-further-as-war-in-the-middle-east-escalates.html

Ministry of Petroleum and Natural Gas, Government of India. (2025). Indian petroleum and natural gas statistics 2024–25. New Delhi: Government of India.

Ministry of Petroleum and Natural Gas. (2025). Mission Anveshan: Seismic survey incentivization programme to enhance exploration and energy self-reliance (Unstarred Question No. 3488). Lok Sabha, Parliament of India.

Oman Ministry of Energy and Minerals. (2020). Ras Markaz crude oil storage and pipeline project. Muscat, Oman.

Press and Information Team of the Delegation to UN and OSCE in Vienna. (2022, April 28). Joint comprehensive plan of action (JCPOA). European External Action Service. Retrieved on March 22, 2026 from https://www.eeas.europa.eu/delegations/vienna-international-organisations/joint-comprehensive-plan-action-jcpoa_en

Ramsay, G., & Said-Moorhouse, L. (2026, March 19). Why the South Pars gas field shared by Iran and Qatar matters. CNN. Retrieved on March 15, 2026 from https://edition.cnn.com/2026/03/19/middleeast/iran-qatar-south-pars-gas-field-explainer-intl

Ramadhani, R., & Marzaman, A. (2024). Maritime stability in the Strait of Hormuz: Challenges, global impacts, and multilateral diplomacy. HYPOTHESIS: Multidisciplinary Journal of Social Sciences, 3(2), 81–96. https://doi.org/10.62668/hypothesis.v3i02.1293

Rastogi, C. (2016). Changing geo-politics of oil and the impact on India. Indian Journal of Asian Affairs, 29(1–2), 69–84.

Reserve Bank of India. (2018, June 6). Monetary policy statement, 2018–19: Resolution of the Monetary Policy Committee. Retrieved on March 30, 2026 from https://rbi.org.in/commonman/english/Scripts/PressReleases.aspx?Id=2596

Reuters. (2026, March 27). Trump's Iran war pushes India to rekindle old friendship with Russia. Retrieved on April 3, 2026 from https://www.reuters.com/business/energy/trumps-iran-war-pushes-india-rekindle-old-friendship-with-russia-2026-03-27/

Sharma, R. (2026, March 25). India has bought 60 million barrels of Russian oil for April. Bloomberg News. Retrieved on April 3, 2026 from https://www.bloomberg.com/news/articles/2026-03-25/india-has-bought-60-million-barrels-of-russian-oil-for-april

Shen, D. (2012). Blocking the Hormuz Strait – China’s energy dilemma. China Security, 8(1), 1–15.

Talmadge, C. (2008). Closing time: Assessing the Iranian threat to the Strait of Hormuz. International Security, 33(1), 82–117. https://doi.org/10.1162/isec.2008.33.1.82

U.S. Central Command. (2026). Operation Epic Fury: Force posture and operational deployment in the Middle East. United States Department of War. Retrieved on March 15, 2026 from https://www.centcom.mil/OPERATIONS-AND-EXERCISES/EPIC-FURY/

U.S. Energy Information Administration. (2023). The Strait of Hormuz is the world’s most important oil transit chokepoint. Washington, DC: U.S. Department of Energy. Retrieved on April 3, 2026 from https://www.eia.gov/todayinenergy/detail.php?id=52780

U.S. Energy Information Administration (EIA). (2025, February 13). Petroleum liquids supply growth driven by non-OPEC+ producers. Retrieved on March 28, 2026 from https://www.eia.gov/todayinenergy/detail.php?id=64565

United States Government. (2025, August 6). Executive order imposing additional tariffs on imports from India in response to purchases of Russian oil. Washington, DC.

Varghese, J. (2026, March 3). Drones hit fuel tank at Oman port: State media. The Hindu. Retrieved on March 14, 2026 from https://www.thehindu.com/news/international/drones-hit-fuel-tank-at-oman-port-state-media/article70698772.ece

Yadlin, A., & Guzansky, Y. (2014). The Strait of Hormuz: Assessing and neutralizing the threat. Institute for National Security Studies (INSS), Tel Aviv, Israel: Institute for National Security Studies.